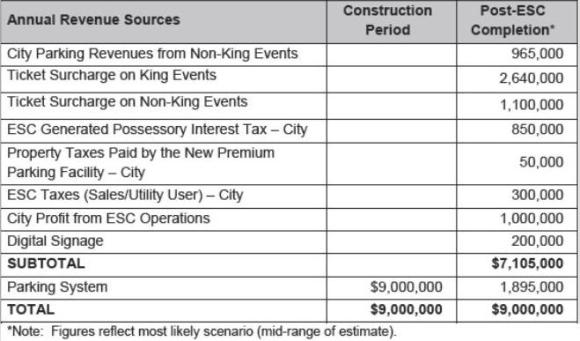

The table above is from page 21 of the

Term Sheet.

It shows the source of backfill for the loss to the general fund that will occur as a result of the sale of the city’s parking assets.

It contains no explanation for how the figures were reached.

Thus, my goal here is to try and determine how realistic these figures are.

City Parking Revenues from Non-King’s Events ($965,000): It is unclear where this figure is derived from, we do not know how many non-King’s events will occur each year, how much parking will cost and how many parking spaces are in play. It is clear is that this amount is dependent upon non-King’s events being well attended, thus this number could fluctuate greatly from year-to-year.

Ticket Surcharges on King’s Events ($2,640,000): This is where it gets interesting.

Michael Shaw from the Sacramento Business Journal

did the math (in reverse) to determine how many people the city assume will attend an average King’s game and how much they will pay for their ticket.

The “the average paid attendance estimate is 16,268 fans or 87.9 percent of the 18,500-seat venue” and the average ticket price is $77.96.

The Kings averaged

15,117 fans in attendance for each season between 2004/2005 and 2010/2011.

This is 1,150 less fans than the cities estimate and includes the 2004/05, 2005/06 and 2006/07 season which were all sold out because the Kings were a competitive team.

For the past four seasons, as the Kings have become a non-competitive team, attendance has dropped dramatically to an average attendance of only 13,466, or 2,802 less than the cities estimate.

Currently an average ticket for an NBA game sells for

$48.48 that is $29.48 or 38% less than the city believes the Kings will be able to charge for an average ticket at the new arena.

To say that the cities attendance and ticket assumptions are optimistic is an understatement.

It is unlikely the Kings, in their current state of perpetual mediocrity, will be able to draw 16,268 fans a game or charge an average of $77.96 for that ticket.

Chicago, Boston and Miami all extremely popular teams in large markets do not even command that type of

ticket price.

Let’s plug some more realistic numbers into the equation to determine how much general fund backfill can actually be expected from the ticket surcharge on King’s events.

Average attendance of 16,117 (I added on a thousand fans because the new arena may boost attendance, at least for the first season) and an average ticket price of $60 (again I added on a bit of a premium for the newness of the arena).

16,117 * ($60 * 5%) = $48,351 in revenue per game.

$48,351 per game *41 games/season = $1,982,391.

$1,982,391 is $657,609 less than what the city is predicting, a significant difference, and that is with the caveat of using optimistic figures. If we use average figures the situation becomes even worse, with the surcharge only generating $1,502,387.93 or $1,137,612.07 less than the city is predicting.

The arena Term Sheet claims that generating $2,640,000 reflects the “most likely scenario,” based on my calculations above that scenario is at best unlikely, and at worst a complete work of fiction.

Ticket Surcharges on Non-King’s Events ($1,100,000): Like the parking revenue from non-King’s events it is unclear where this figure is derived from because we do not know how many non-King’s events will occur each year and how much the average ticket price is. It is probably safe to assume the figure is too high because the figure for revenue generated from the ticket surcharge on King’s events is far too high. It is certainly clear is that this amount is dependent upon non-King events being well attended and the number could fluctuate greatly from year-to-year.

The ESC Generated Possessory Interest Tax – City ($850,000): The agreement states “[o]nly the city portion of the possessor interest tax would be used for backfill of the General Fund.” I am not sure exactly how to read this but it appears to me the city is paying tax to itself, I’m not really sure how this would be considered a new source of revenue to backfill the general fund.

Property Taxes Paid by the New Premium Parking Facility – City ($50,000): Devin Lavelle

points out that while this is a new source of revenue, the amount of property tax would likely be more if the land was used for another kind of development because

“[a] parking lot has a lower property value than retail or housing that would otherwise be there.”

ESC Taxes (Sales/Utility User) – City ($300,000): As with the possessory interest tax it appears that at least a portion of the new Utility User tax is the city is paying tax to itself.

The sales tax generated is not a new source of revenue because it is just replacing the sales tax currently being collected at Arco Arena.

City Profit from ESC Operations ($1,000,000): This appears to be a legitimate source of new revenue. Although I do not know if the city currently makes any money from Arco Arena, if they do then this revenue would just replace revenue that is lost when Arco Arena is closed.

Digital Signage ($200,000): This is a legitimate new source of revenue.

Parking System ($1,895,000): I am not really sure what this amount is, since the assumption is that, the city will be selling its parking assets. My best guess is that this is money left over after the parking has been sold and the arena has been built. I have serious doubts that any money would actually be left over.

Based on the above analysis the amount of general fund backfill listed in the Term Sheet is entirely too high. A number closer to $6.5 million seems much more realistic and that is with giving the benefit of the doubt to the City on a lot of the numbers presented. The City Council and Taxpayers need raise some serious questions about the figures presented in the Term Sheet and how realistic they are.

Just to be clear, I am not a financial analyst by trade, just a concerned citizen attempting to make sense out of the sparse and confusing information being by presented by the City.

{kind=link}